THE EVOLUTION OF THE OFFICE SECTOR

The ‘Office’ has featured heavily in the press over the past 18 months and indeed in everyday conversation, as working from home became a necessity for most office-based employees. Countless articles and blogs have been published with sensationalised headlines such as “What will the office market look like after the great remote working experiment?” to “Productivity of remote workers could determine the fate of the office market”.

Our view is that the office will now assume a wider function with a more consolidated, improved, and focussed environment to manage the challenges of hybrid working and employee engagement going forward.

Over the last 6 years, Irish office developments have evolved considerably with numerous exceptional schemes being delivered. These buildings have attracted leading global firms to Dublin in particular and the expansion of many more as they continue to increase their presence and EMEA HQs. Due to the new standards set by these firms, occupier expectation has increased which has resulted in developers placing more emphasis on emulating what the tech sector has traditionally offered to their employees: amenity, a perk, a perceived life work balance. They have achieved this through the accumulation of amenity-based facilities such as: high end shower and bicycle facilities, concierge services, tenant events, better reception areas, coffee docks and townhall spaces. This together with improved building standards and environmental and sustainability credentials coming more to the fore has given rise to the creation of world class and award-winning office buildings in Ireland.

However, the office sector is about to enter a new phase. Traditionally offices required a centralised location which has been challenged by technology. Prime offices were traditionally clustered around transport infrastructure in a central business district where multiple advantages of proximity to transport, telecommunication infrastructure and labour combined to attract a premium from occupiers, but technology is challenging the need for multiple office functions to take place in a centralised location. This need must be replaced with desire. The user of the building now places more focus on it being a positive environment for their business and their teams.

Like the revolution that has taken place in the retail market where the ability to shop online challenged traditional assumptions on the functionality of real estate, investors in the office sector must adopt an experience focussed strategy. The nascent breakthroughs the sector has made recently to enhance user experience must be expanded upon, implemented at an early stage in the development process and maintained through a proactive management regime.

As real estate’s function evolves, how do we deliver a successful solution for this next phase in the evolution of the office? As mentioned previously User experience is key and this can be achieved through many innovations. These changes do not have to be seen as challenges but as opportunities to be proactive and differentiate a proposition from that of their competitors.

Through Bannon’s extensive property management portfolio and experience in working as design consultants on several large new schemes, our role in working with investors and developers on identifying and enhancing the user experience for office occupiers and their teams has come into sharp focus.

For the investor the asset cannot be just about place making or achieving optimal rental outcome. An investor must consider it as a longer-term play by exploring tenant optimisation i.e. perhaps leasing a portion of the scheme at lower rents to amenity-based occupiers to carefully coordinate a desired aspirational environment. Correct implementation of property and asset management functions is fundamental, they are key to ensuring the functionality for their occupiers from both a corporate and personnel perspective. Communication with occupiers is essential as creating positive experiences for users of the buildings will in turn lead to greater loyalty and enhanced values.

As we move closer to a return to the office in whatever form, recruitment and retention will continue to be the driving force in office acquisitions. Therefore, to adapt to a hybrid model, promote productivity and engage with the ‘new employee’, the office needs to evolve to reflect what people want to use every day. The era of passive office investment is over.

Lucy Connolly is a Divisional Director at Bannon. She has 15 years’ experience acting for a wide variety of private clients and companies in relation to commercial property, office acquisitions, sales and lettings. Contact Lucy by email on lconnolly@bannon.ie

The function of all forms of real estate and the specific requirements of its users continues to change at pace. The most significant factors driving this evolution are non-financial – Environmental, Social and Governance (ESG) requirements.

The function of all forms of real estate and the specific requirements of its users continues to change at pace. The most significant factors driving this evolution are non-financial – Environmental, Social and Governance (ESG) requirements.

culture of the market and understand the importance of real estate delivering long term returns for our clients. However, we believe this can be done in a way that simultaneously creates better places to work and reduces the impact on the environment.

culture of the market and understand the importance of real estate delivering long term returns for our clients. However, we believe this can be done in a way that simultaneously creates better places to work and reduces the impact on the environment.

Dublin Town reporting footfall in the City Centre at 87% of 2019 levels last Saturday, given the lack of Tourists that’s a very encouraging recovery. It will be interesting to see which retailers benefit most from the return of the consumer.

Dublin Town reporting footfall in the City Centre at 87% of 2019 levels last Saturday, given the lack of Tourists that’s a very encouraging recovery. It will be interesting to see which retailers benefit most from the return of the consumer.

Following the government’s transposition of IORP II, any new One Member Arrangements (OMA) will now be largely prevented from borrowing for their investments and be required to hold at least 50% of their investment in regulated markets e.g. listed shared and/or bonds.

Following the government’s transposition of IORP II, any new One Member Arrangements (OMA) will now be largely prevented from borrowing for their investments and be required to hold at least 50% of their investment in regulated markets e.g. listed shared and/or bonds.

After the pandemic: in Dublin’s bare city. Our streets must be reimagined to entice visitors rather than cater to workers. Bannon advises on this in

After the pandemic: in Dublin’s bare city. Our streets must be reimagined to entice visitors rather than cater to workers. Bannon advises on this in

Last minute residential deal tips market over €3bn.

Last minute residential deal tips market over €3bn.

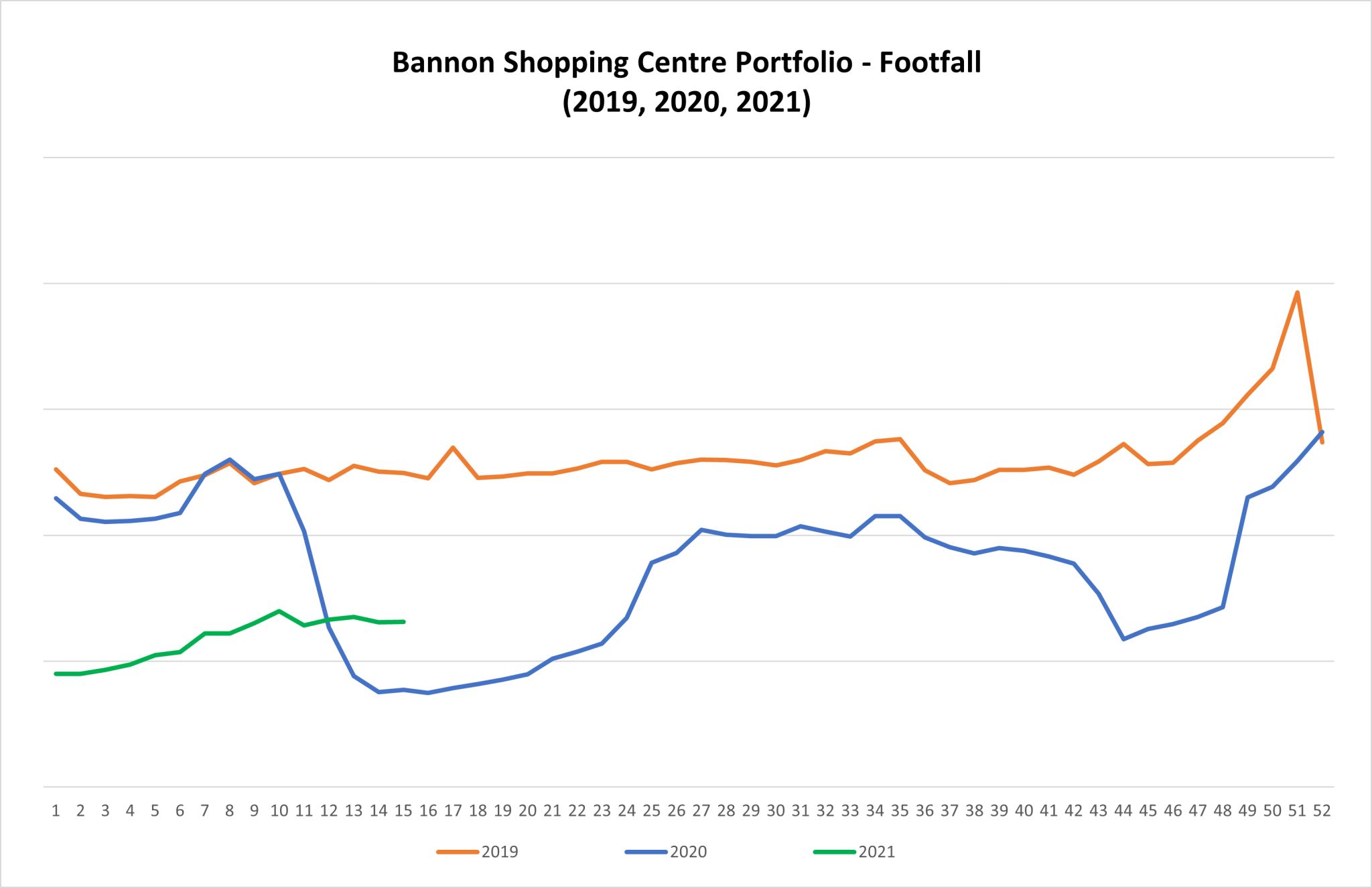

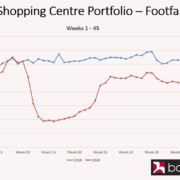

In general the footfall across our portfolio is remarkably consistent every year, however 2020 is very different. We remain hopeful that people will shop with purpose when the restrictions are eased at the start of December.

In general the footfall across our portfolio is remarkably consistent every year, however 2020 is very different. We remain hopeful that people will shop with purpose when the restrictions are eased at the start of December. The inconsistent and illogical nature of the imposition of essential goods only sales in retail across the country is causing serious damage to the sector.

The inconsistent and illogical nature of the imposition of essential goods only sales in retail across the country is causing serious damage to the sector.

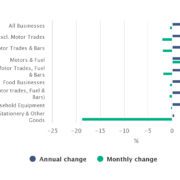

The volume of retail sales decreased 0.5% in October when compared to September on a seasonally adjusted basis and increased by 3.0% on an annual basis. When Motor Trades are excluded, the volume of retail sales decreased by 2.1% in October 2019 and rose by 3.2% when compared with October 2018.

The volume of retail sales decreased 0.5% in October when compared to September on a seasonally adjusted basis and increased by 3.0% on an annual basis. When Motor Trades are excluded, the volume of retail sales decreased by 2.1% in October 2019 and rose by 3.2% when compared with October 2018.

The volume of retail sales increased 4.3% in September when compared to August on a seasonally adjusted basis and increased by 4.2% on an annual basis. When Motor Trades are excluded, the volume of retail sales increased by 2.3% in September 2019 and rose by 4.7% when compared with September 2018.

The volume of retail sales increased 4.3% in September when compared to August on a seasonally adjusted basis and increased by 4.2% on an annual basis. When Motor Trades are excluded, the volume of retail sales increased by 2.3% in September 2019 and rose by 4.7% when compared with September 2018.

Smyths, meanwhile, has completely conquered the British market, opening more than 100 large retail outlets there in a little over a decade, vanquishing its specialist rivals. Its UK sales are now about €675 million.

Smyths, meanwhile, has completely conquered the British market, opening more than 100 large retail outlets there in a little over a decade, vanquishing its specialist rivals. Its UK sales are now about €675 million.