The Irish economy looks set to register strong growth again in 2019 with GDP likely to increase by almost 6 per cent in the current year. While certain multi-national related transactions are distorting the headline figures, the large increase in taxation receipts and the continued strong performance of the Irish labour market means the underlying economy is performing well.

The persistent growth of the Irish economy is remarkable given the strong headwinds observed in 2019, the uncertainty about the Brexit process, and the moderation observed in global conditions, all of which are likely to have had a negative impact on the domestic economy. The Brexit process has merely been parked, with the possibility of a free trade agreement being negotiated between the UK and the EU in 2020. This will almost certainly result in further uncertainty in the years ahead. We expect to see the economy grow by a slower rate in 2020 of 3.3 per cent.

Another potential challenge for the Irish economy is the issue of corporation tax receipts, which are becoming an increasingly large share of the total tax receipts of the Irish exchequer. They now account for over 18 per cent of total tax receipts and there is concern that a portion of these receipts may be windfall revenues, which are not sustainable. ESRI economist Petros Varthalitis examines the implications for key fiscal metrics if there was a sudden reduction in the amount of corporation tax receipts available. It would likely require significant measures to be adopted by the Government in order to maintain fiscal discipline. The results underpin the need to quantify the potential windfall component of these receipts. They are also important given the recent proposals by the OECD for corporation tax policy.

The Commentary also examines the regional diversity of the Irish property market performance over the last 10 years. ESRI economists Matthew Allen-Coghlan and Kieran McQuinn note that both prices and rents have grown at significantly different rates in different areas of the country during this period. Areas of the country that had relatively high prices and rents initially experienced the fastest pace of growth subsequently. This suggests that different regions of the country have experienced varying economic growth rates over the past 10 years.

ESRI reports

As per the Retail Sales figures released by the CSO and our own experience across our retail park portfolio DIY & Household goods sales have been the stand out performer of the Retail sector since March.

As per the Retail Sales figures released by the CSO and our own experience across our retail park portfolio DIY & Household goods sales have been the stand out performer of the Retail sector since March.

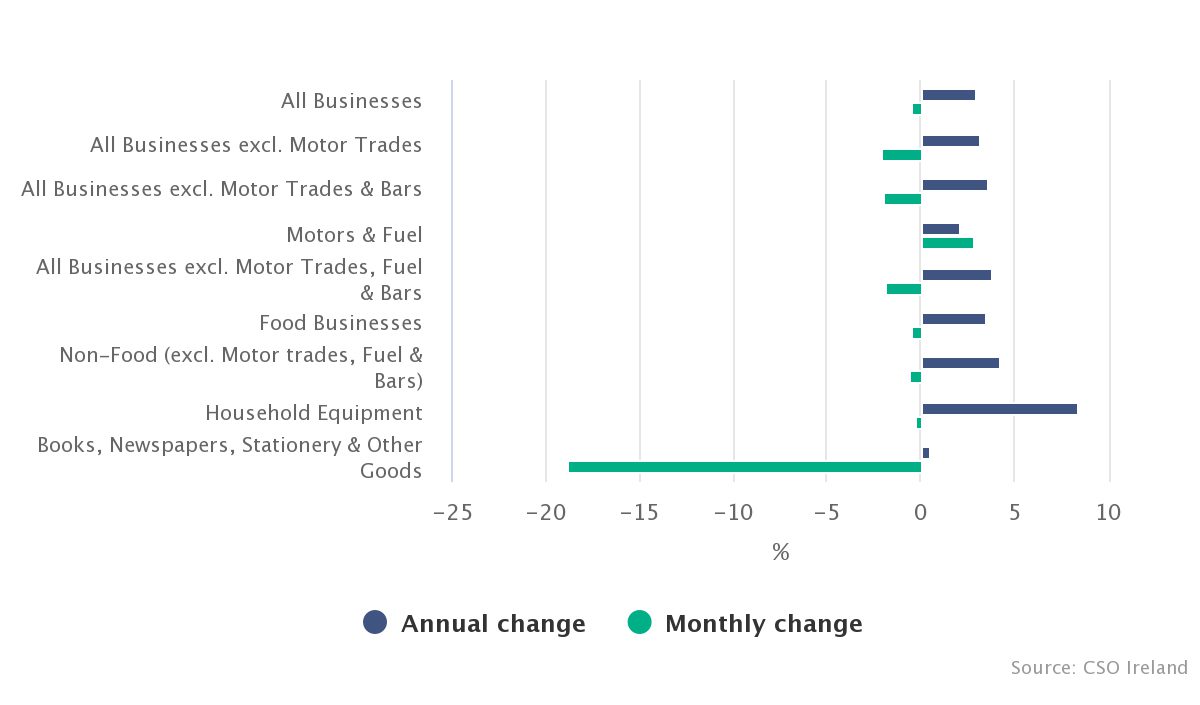

The volume of retail sales decreased 0.5% in October when compared to September on a seasonally adjusted basis and increased by 3.0% on an annual basis. When Motor Trades are excluded, the volume of retail sales decreased by 2.1% in October 2019 and rose by 3.2% when compared with October 2018.

The volume of retail sales decreased 0.5% in October when compared to September on a seasonally adjusted basis and increased by 3.0% on an annual basis. When Motor Trades are excluded, the volume of retail sales decreased by 2.1% in October 2019 and rose by 3.2% when compared with October 2018.