Despite retail sales statistics showing a sluggish performance, estate agents report increased activity by retailers and this is reflected in falling vacancy levels in shopping streets and centres.

Agents differ about the impact of Brexit. Marie Hunt of CBRE acknowledges a noticeable increase in cross-border shopping in some border towns in July and August following the weakening of Sterling but says that Irish consumers don’t appear to have curtailed spending in the aftermath of Brexit.

However, another agent says that some UK fashion retailers have pulled back from their Irish expansion plans or put them on hold following Brexit. They are expected to monitor future indices from the Central Statistics Office to see how retail sales trends develop.

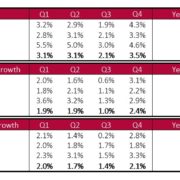

In July retail sales in the Republic fell 0.5% when compared with June this year after car sales are excluded. The worst affected shops were clothing, footwear and textiles down 2.5%. Other retail sales were down 2.4% and food, beverages and tobacco were down 0.9%.

Neil Bannon of Bannon points to the other retail sectors that showed continued growth in July, notably furniture and lighting up 5.3% and books, newspapers and stationery up 2%. Furthermore, while the fashion sector fell in both July and June, over the three months including May, fashion sales are 8.7% ahead of the corresponding three months of 2015. All businesses excluding motor are 4.6% ahead.

“We don’t need spectacular growth because there’s always a fear that such growth cannot be sustained. It’s better to have a solid, steady performance,” says Neil Bannon.

Bannon’s agency manages 40 shopping centres in Dublin and around the country and are letting agents on about a quarter of the market. He says there has been a consistent improvement in the retail sector since September 2013.

“It’s not just Dublin; it is also happening around the country on the back of the growth in employment,” he says, and instances Athlone Town Centre where Marks and Spencer are anchors. “This centre has shown retail turnover increase more rapidly than footfall,” Bannon adds.

Other healthy signs have been the drop in examinerships as well as reduced vacancy levels, as the last 12 months have seen the re-emergence of retailer demand for space.

He cites the example of a shop in a north Dublin suburb that had been vacant for almost 10 years and even after the landlord had dropped his asking rent to €20 per sq.ft there were still no takers. Then this year three retailers expressed an interest and made offers, with the highest being 20% more than the rent they would have paid for it last year.

Lisney’s most recent retail report suggests that with increased competition from retailers for vacant space, some landlords have become more choosy about the tenants they are willing to accept for premium retail outlets.

Earlier market indicators suggested that premiums for leases were going to make a comeback this year, particularly on prime shopping streets. However, it would appear that while there are retailers in the market willing to pay premiums in order to acquire prime units, landlords are often not willing to accept them as tenants due to the proposed use (or the quality of their track record).

Lisney’s Emma Coffey says the food sector is driving demand in the city centre, with restaurants and coffee shop operators actively seeking properties in Dublin 2, 4 and 6. However, there was little or no stock available for them to choose from. “In some areas such as Wicklow St, retailers are willing to pay key money. In other areas the demand is not that strong,” says Coffey.

Furthermore, there have been signs that some UK retailers and some restaurant owners are showing resistance to higher rents and requests for key money.

A CBRE survey shows that prime Dublin retail rents have risen almost 39% since the crash. While this places them ahead of all the UK’s regional cities such as Birmingham and Manchester, nevertheless these rents are very much in the middle ranks in European cities.

Neil Bannon says that such higher rent arise because others are competing to get the space.

One area of Dublin that looks set to get a retailing boost in the near future is the eastern side of O’Connell St. Traditionally the western Henry St side, with its large fashion stores, is the favoured side of the street. But with the Luas extension scheduled to travel down Marlborough St and with Mike Ashley’s Sports Direct purchasing Boyers department store on North Earl Street for a reported €12m, the street’s eastern side and nearby retail premises may attract increased interest from a greater range of retailers.

An interesting test of the north city market will be seen when Kennedy Wilson completes the sale of its 3 mobile phone store on Henry St, for which it is asking €8.25m. Its current rent roll is €425,000, suggesting a net initial yield of 4.93%.

Ciara Connolly of Cushman & Wakefield’s retail department says some fashion chains are expanding both within and outside of Dublin. She instances Quiz, which has 10 stores in Northern Ireland and which in the last 12 months has opened in Liffey Valley, Blanchardstown and ILAC in Dublin as well as Douglas in Cork and Crescent in Limerick.

The Bestseller chain, which includes the Jack and Jones, Dila and Selected brands, is also active. Its Selected chain has opened in Dundrum and is looking for stores in Cork and Limerick. The Inditex group, whose Zara brand is long established in Ireland and which last year opened a Massimo Dutti store on Grafton St, is looking to expand its younger fashion brands, especially its Stradavarius and Bershka in new locations. Meanwhile, its Zara Homes is looking at the Grafton St area for a possible new store.

Report in the Independent